Insurance

How to Get Car Insurance: 6 Steps to Get the Coverage You Need

How Does Car Insurance Work — and What Does It Cover?

Buying a new car, whether it’s fresh out of the factory or just new to you, can be exciting. However, you want to be sure you have all your required documentation in order so you can drive off the lot with as few hiccups as possible.

Making sure you have the right insurance coverage for your needs and per your state’s requirements is part of that process. Not only will this help you leave the lot in a timely fashion but it will also protect you once you drive away in your new car.

Whether you’re buying a car or just want to save money on car insurance, here’s how to get car insurance coverage.

In this article

- What types of car insurance do you need?

- How to get car insurance

- The final word on car insurance

What types of car insurance do you need?

Although each state has its own car insurance minimums, almost every state requires drivers to have at least some form of auto insurance. Even if car insurance isn’t mandatory in your state, such as New Hampshire and Virginia, you may need to pay a fee or meet other financial criteria if you choose not to have it. In general, car insurance is usually a good investment.

Here are the typical components of an auto insurance policy. Use this information, along with your state’s required limits, to determine the coverage you need.

Liability coverage

Auto liability coverage is required in most states, though the minimum amount of liability coverage you’re legally obligated to purchase varies from state to state. Liability coverage has two components:

Bodily injury liability

Bodily injury liability coverage pays damages if you’re responsible for another person’s injury or death in a car accident. It also pays for your legal defense if you’re sued as a result of an accident. If the damages are high, all of your assets — your home, savings, and future wages — could be in jeopardy.

When you purchase bodily injury liability coverage, you select two limits. For example, $250,000/$500,000. The first number in the coverage limit is the maximum for any one person; the second number in the coverage limit is the total for one accident. When selecting bodily injury liability coverage, you should try to buy enough to fully protect your assets.

Property damage liability

If you’re in a car accident and are liable for the damage to another person’s property, property damage liability coverage will pay for the damage up to your chosen coverage limit. It also covers your legal defense if you’re sued as a result of an accident.

Property damage can include damage to another person’s car, a building, a fence, etc. When choosing your coverage, select the most coverage you can afford. The minimum requirement varies by state but ranges anywhere from $10,000 to hundreds of thousands of dollars.

Personal injury protection

Personal injury protection, or PIP, is no-fault insurance that can help pay your and your passengers’ medical expenses if you’re injured in a car accident. It pays regardless of who caused the accident. PIP is not available in all states, but it’s required in some and optional in others.

The level of benefits can vary by state, but coverage typically includes medical, disability, and death benefits. When choosing PIP, you select the deductible you want to pay, which will impact your insurance premiums.

Uninsured and underinsured motorist coverage

If you’re hit by a driver who isn’t insured or whose insurance doesn’t cover the cost of your resulting medical bills, uninsured and underinsured motorist coverage may help.

Depending on your state, these coverages may be mandatory or optional. They may also be combined, or you may have to purchase them separately.

Uninsured motorist coverage

Uninsured motorist coverage pays out if you or your passengers are injured in an accident caused by an uninsured motorist. In other words, this coverage takes the place of bodily injury liability coverage that the other driver should have purchased but did not.

Underinsured motorist coverage

Underinsured motorist coverage pays you for damages resulting in bodily damage from an accident caused by a motorist whose liability coverage limits are insufficient to cover your claim.

Medical payments coverage

Medical payments coverage, or MedPay, covers the cost of medical expenses such as ambulance, surgery, X-rays, and physician costs, regardless of who was at fault in the accident.

MedPay also covers the cost of funeral expenses for you or others killed in an accident. MedPay is similar to PIP, though it’s optional and not available in every state. MedPay can supplement your health insurance coverage.

Comprehensive coverage

Comprehensive coverage pays for damage to your vehicle caused by nearly everything else other than collision. This includes damage caused by theft, vandalism, fire, flooding, and so on.

When choosing this coverage, you’ll select the deductible you’ll pay if you file a claim. Comprehensive coverage is optional in all states; however, if you finance your car, your lender may require it.

Collision coverage

Collision coverage pays for damages caused by a collision or when your vehicle overturns. Similar to comprehensive coverage, collision coverage isn’t required by law; however, your lender may require it if your car is financed.

Other types of auto insurance coverage

Emergency road service

Covers towing, jump-starts for a dead battery, labor for flat tires, etc., and is optional.

Rental reimbursement

Rental reimbursement pays for a rental car if your vehicle is damaged as a result of a covered loss. You choose how much you want to pay for each day of having the rental car and a total maximum.

When Life Insurance Is Worth the Cost — And How to Get Coverage

GAP coverage

GAP insurance covers the difference between what you owe on your car and the car’s actual cash value in the event your insured car is totaled in an accident.

How to get car insurance

There’s no shortage of car insurance companies out there, which means you have plenty of options to find the auto policy that’s right for you. Here are some steps to make sure you’re getting the best car insurance.

1. Do the research

Take the time to find the best companies and what special services and discounts they offer that you can benefit from. If you cherish stellar customer service and find a particular company is riddled with negative reviews, it may not be worth it to get a quote from them.

2. Determine how much coverage you need

Before buying car insurance, determine how much coverage you need. This may feel like the hardest part of the process, but a general rule of thumb is to purchase as much coverage as you can afford so that you’re adequately covered. Familiarize yourself with each component of car insurance coverage outlined above to help make this decision.

3. Shop around and get your free quotes

Most car insurance companies provide free car insurance quotes, which you can get either online or by calling and speaking with an agent directly. Either way, you typically need the following information on hand:

- Names, dates of birth, driver’s license numbers, and Social Security numbers of all people on the policy

- VINs (vehicle identification numbers) for all vehicles you want covered

- The declarations page from your most recent prior car insurance policy

4. Or use an insurance marketplace instead

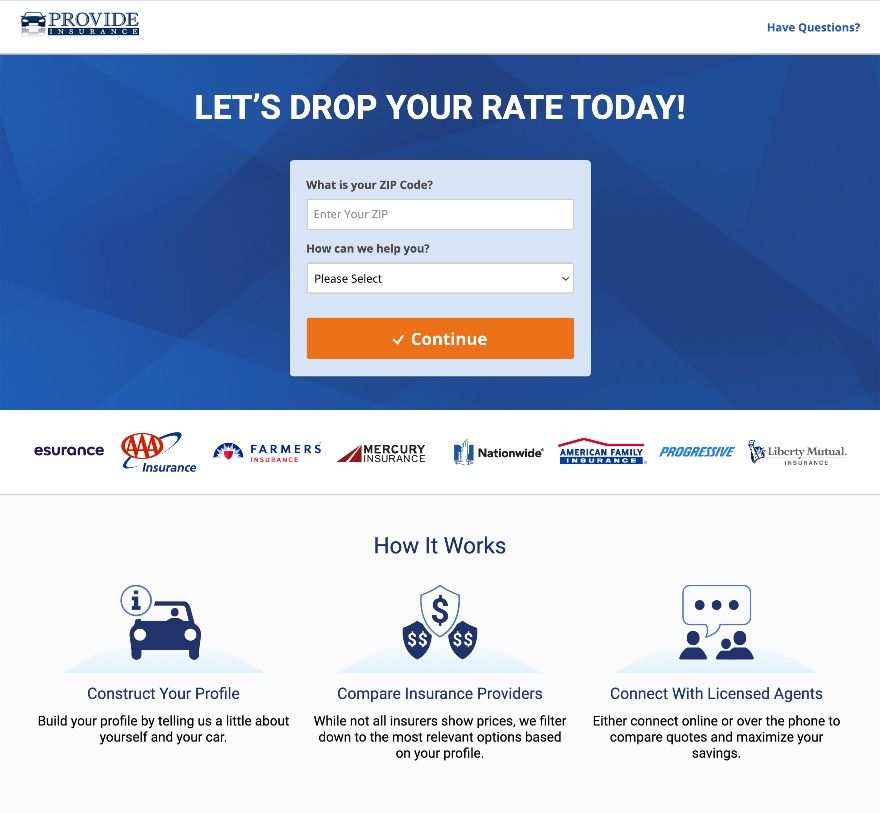

Alternatively, you can use a car insurance marketplace such as Provide Insurance to compare quotes. Provide Insurance is a free way to get a variety of auto insurance quotes from several leading insurance agents all at once. Don’t feel like entering the same information over and over again with several car insurance agents? Provide Insurance may be the way to go.

Let’s say you’re currently insured, but want to find a way to save money. Here’s how to save with Provide Insurance:

- Step 1: Navigate to Provide-Insurance.com. Once on the homepage, enter your zip code and choose “Currently insured, need savings” from the drop-down menu. Then, click continue.

- Step 2: After clicking continue, a new window will open and you’ll see a bar at the top that tracks your progress. From here, go through each question, providing all necessary information about your vehicle. This includes your vehicle year, make, model, whether you own, finance, or lease your vehicle, mileage, and how much coverage you need.

- Step 3: After entering your vehicle information, you’ll be asked to provide your current insurer. Select the company from the list and how long you’ve continuously had car insurance.

- Step 4: Next, select how many drivers you want on the policy, your gender, marital status, education level, occupation, and credit score.

- Step 5: The next few questions ask about your driving record. This includes things like at-fault accidents and tickets you’ve had in the past three years, as well as any DUIs and whether you’ve had your license revoked in the past three years.

- Step 6: If you’ve chosen to add a second driver to your policy, the next few screens will ask for their relation to you. You’ll also need to provide their gender, education level, occupation, driving record information, and age.

- Step 7: Next, you’ll need to enter whether you own or rent your home. From here, you can choose whether you would like to receive home or renter’s insurance quotes in addition to your car insurance quote.

- Step 8: As you progress through the remaining questions, you’ll be asked for your personal information such as military service, date of birth, your name and the names of any other drivers on the policy, street address, and email. Lastly, enter your phone number and click “Show My Quotes.”

The final screen will populate your car insurance quotes from several providers. Click through to view each quote and select the one that best fits your needs.

5. Pick a car insurance company and get insured

Once you’ve reviewed your coverage options and found an affordable car insurance rate, it’s time to decide on a company and get insured. Read your policy documents before and after you sign, ensuring the information is correct before and after you purchased the policy.

6. Cancel your old car insurance policy

With your new policy in place, go ahead and cancel your old one. Make sure you wait until you’re covered by your new policy before canceling your old policy so your coverage doesn’t lapse.

The final word on car insurance

Even if car insurance isn’t required in your state, it’s a good investment. Take the time to determine how much protection you need and compare policies across different car insurance companies.

Car accidents can result in a tremendous financial burden for motorists without sufficient coverage. Consider purchasing as much coverage you can afford. That way, you’re not only adequately protected, but also have peace of mind.

>>Click here for your free insurance quote

Save $500 A Year

Get a quote now

Get a quote now

- Save up to $500 a year on your car insurance

- Compare dozens of providers in under 5 minutes

- Fast, free and easy way to shop for insurance

- Quickly find the perfect rate for you

Get a quote now

7 Types of Insurance Coverage You Need (And 3 You Might Want)

Refinancing an Auto Loan: How to Know If It’s a Good Idea

Reverse Mortgages Pros and Cons: Ripoff or a Good Idea?

8 Ways it Just Got Easier to Achieve Student Loan Forgiveness

15 Smart Strategies for Planning a Move During COVID-19

Term vs. Whole Life Insurance: Why Term is Almost Always Better

PrivacyGuard Review

Orchard Bank Credit Cards | NOT a Scam!

What is CitiCards CBNA On My Credit Report

What is BRCLYSBANKDE on My Credit Report?