Credit

What Credit Score is Needed to Buy a House?

Have you ever wondered why what credit score is needed to buy a house is such a popular topic among homebuyers?

It’s not just about whether or not you’ll be approved for a loan to buy the house of your choice. Just as important, it’s about how much you’ll pay for that home each and every month.

Your credit scores are a major part of the calculation that will determine what interest rate you’ll pay on your mortgage, in addition to your ability to even be approved.

But apart from the interest rate, your credit score can also affect another important part of your monthly payment, which is any mortgage insurance that may be required by the lender to make the loan.

Once you’ve read this article, you’ll have all the incentive needed to put in the time and effort to maximize your credit score to buy a house. Get it right, and you can save yourself thousands of dollars each year, and tens of thousands of dollars over the life of your mortgage.

Table of Contents:

- What Credit Score Do You Need To Buy a House?

- The Effect of Your Credit Score on the Interest Rate You’ll Pay

- The Private Mortgage Insurance Factor

- Improving Your Credit Score Before Applying For A Mortgage

What Credit Score Do You Need to Buy a House?

Credit scores can range between a low of 300 to a high of 850. If you’re applying for mortgage financing, you’ll need to meet a minimum credit score requirement based on the type of loan you’re applying for.

There are five primary general mortgage programs, each with their own credit score requirements.

Credit Score Needed According to Loan Type:

- Conventional: With a conventional home loan, the minimum is usually 620, but it may be higher if you’re purchasing a vacation home or an investment property.

- FHA: With a typical down payment of 3.5% the minimum score is generally 580. But if you make a down payment of 10% or more, FHA will permit a credit score as low as 500.

- VA: The Veterans Administration doesn’t impose a minimum credit score. However, lenders will typically set a minimum credit score of 620, though some will go as low as 580.

- Jumbo: These are for larger loan amounts on higher-priced properties. Since they’re issued by private sources, typically banks, credit scores will vary with each individual program. 620 is likely to be the absolute minimum, but many may set a higher threshold, like 660 or even 680.

- USDA: Like VA mortgages, USDA mortgages don’t have a fixed minimum credit score. However, to get a standard approval – which is the easiest to qualify for – the minimum credit score is 640. Lower scores are permitted under certain circumstances, and with required documentation.

Second mortgages, home equity loans and home equity lines of credit (HELOCs) are issued by banks and credit unions. Each set their own credit score minimum.

While it’s possible you may get secondary financing with a score as low as 620, it’s more likely the minimum will be higher, like 660 or 680, because secondary financing is riskier to lenders than first mortgages.

The Effect of Your Credit Score on Interest Rates

In the previous section, we discussed minimum credit scores to qualify for a mortgage. Those score thresholds refer to the minimum score at which your loan is likely to be approved.

Assuming you at least meet the minimum score requirement, the exact level of your credit score can have a major impact on the interest rate you’ll pay on your loan.

This is especially true of conventional mortgages, jumbo mortgages, and secondary financing. Each involves what’s known as tiered pricing, which is to say your loan rate will be determined by a combination of factors.

Those will include your loan-to-value ratio (the amount of the loan divided by the property value), the type of loan (fixed or adjustable), and your credit score.

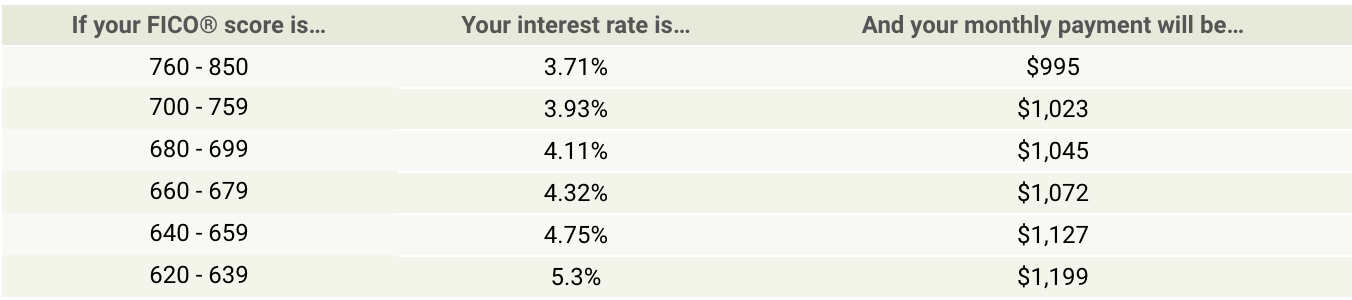

According to myFICO.com, interest rates and monthly payments on the same loan amount can vary substantially at different credit score levels (rates current as of 3.24.2020):

In looking at the screenshot above, you can see that an applicant with a fair credit score of 630 will pay more than 1.5 points higher on the rate than someone with a credit score of 800.

That will translate into a difference in the monthly payment of nearly $200, or $2,400 per year. Over 30 years, the difference will be a staggering $72,000.

As you can tell, getting a mortgage with a bad credit score can really impact the amount of money you owe on the overall life of the loan.

But where credit scores are concerned, interest rates aren’t the only cost they can affect.

The Private Mortgage Insurance Factor

Conventional and jumbo mortgages require that you pay private mortgage insurance (PMI) anytime you make a down payment of less than 20% of the purchase price of a home, or if you refinance your home in an amount that exceeds 80% of the property’s appraised value.

PMI is not to be confused with mortgage life insurance, which pays off the mortgage upon the death of the homeowner. Instead, PMI pays the mortgage lender if the homeowner defaults on the mortgage. Though it doesn’t pay the entire amount of the loan balance, it pays a percentage that lowers the effective loan-to-value on the property for lending purposes.

For example, a mortgage that equals 95% of the value of the securing property may have a PMI requirement of 30%, which reduces the effective loan-to-value down to about 68%. Should the borrower default, the lender will be highly likely to recover the full amount of the outstanding loan balance from a combination of the sale of the property and the insurance paid by the PMI provider.

PMI is essentially an insurance policy paid by the borrower that provides the lender an inducement to approve a loan that might otherwise be considered too risky.

PMI Example with Two Different Credit Scores

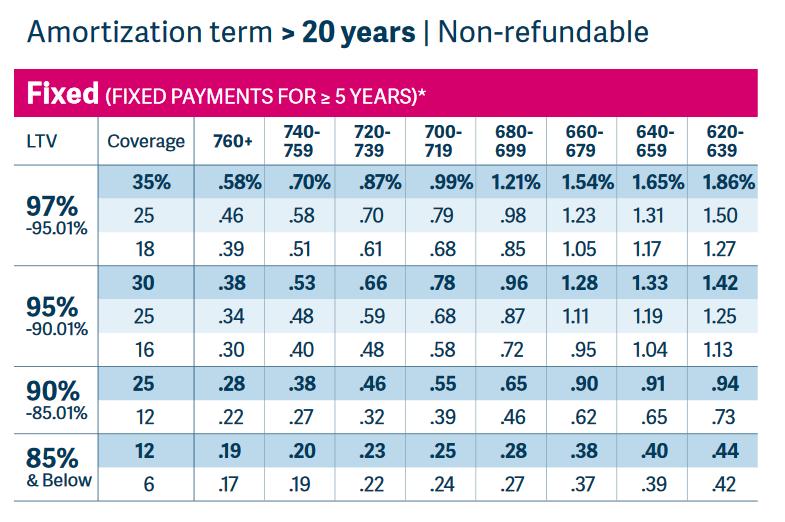

Like interest rates, PMI rates are heavily influenced by your credit score. The following rate screenshot from MGIC, one of the industry’s most prominent PMI providers, clearly shows the impact credit scores have on the premium you will pay for the coverage:

The screenshot shows the annual premium factors charged on a 30-year fixed rate mortgage based on eight different credit score ranges.

Taking the 95% – 90.01% LTV range at 30% coverage, notice that the annual premium factor for someone in the 740 to 759 credit score range (top row) will have an annual premium factor of .53%, while someone in the 660 to 679 score range will have a factor of 1.28%.

Here’s how much each will add to your monthly payment on a home, assuming a 30-year mortgage for $300,000:

- 740 to 759 credit score range: $300,000 X 0.53/100 = $1,590 per year, or $132.50 per month.

- 660 to 679 credit score range: $300,000 X 1.28/100 = $3,840 per year, or $320 per month.

The borrower with a lower credit score will have a higher monthly payment by $187.50, just from PMI. On an annual basis, that will add $2,250 to the cost of owning the home.

As you can see, a lower credit score can cost you twice when it comes to a mortgage. The first is in the form of a higher interest rate and monthly payment on the loan itself, while the second is from a higher premium for PMI.

In fact, a low credit score can add thousands of dollars per year to the cost of owning a home, so having a good credit score can save you thousands of dollars per year on your home loan.

Improving Your Credit Score Before Applying for a Mortgage

Once you realize the impact your credit score will have on your monthly mortgage payment, you should make every effort to improve your credit score before applying for a mortgage.

Monitor Your Credit

If you’re not already doing so, you should be monitoring your credit score regularly. You can usually do this for free through popular free credit score providers like Credit Karma and Credit Sesame. But it’s likely you already have access to your credit scores through banks and credit unions.

Many now provide them as a free service if you have a deposit account or a credit card with that institution. Find out where your score is right now, and begin tracking it between now and the time you apply for a mortgage.

If you don’t like the score you have, there’s plenty you can do to improve it.

Get a Copy of Your Credit Report

First, get a copy of your official credit reports from all three credit bureaus – Experian, Equifax, and TransUnion. You’ll need all three because mortgage lenders access your credit information from each, so you’ll want to be looking at the same credit reports your mortgage lender will.

Fortunately, you can get a free copy of your credit reports from Annual Credit Report.com. It’s the only source officially authorized to provide you with a copy of each of your three credit reports (there’s one issued by each of the three bureaus).

Once you have it, do a thorough review of your credit report. Pay close attention to any derogatory information. That can include late payments, past-due balances or collections, or legal information, like bankruptcies or judgments.

Get Your Free Credit Report Today

Dispute Negative Information

There’s not much you can do about bankruptcies or judgments since they’re a matter of public record.

But if you see any negative information on your credit report that you believe to be in error, file a formal dispute with that creditor. If you can get the information removed or corrected, which you usually can if you provide a reasonable explanation supported by documentation proving your point, your credit score will improve with each negative entry that’s removed.

If you have any past-due balances or collection accounts, pay them off immediately. Even though they’ll remain on your credit report for several years, a paid account is always better than an open one. Just paying off the balance owed on such an account can raise your credit score several points.

Lower Credit Utilization

One of the biggest factors that may be weighing down your credit score is credit utilization. It’s the amount you owe on loans and credit cards compared to either the high credit limit or the original loan balance.

For example, let’s say you have total credit limits and original installment loan balances of $40,000 (on currently active loans), and you owe $12,000 collectively. Your credit utilization ratio is 30%, or $12,000 divided by $40,000.

30% is considered to be the ratio at which credit utilization begins to have a positive effect on your credit score. You should work to lower the amounts you owe to below 30%. The higher the ratio is, the lower your credit score will be.

At 80% or more, your credit utilization ratio is considered to be a major negative factor. Lowering it is one of the best credit improvement strategies you can employ.

So, What Credit Score Do You Need To Buy A House?

As you can see, one of the most important strategies you can use to improve the affordability of the next house you buy is to improve your credit score.

Though there are definitely certain minimum credit scores to buy a house, you don’t want to go into the application process with just the minimum.

In fact, you shouldn’t even go in with the average credit score to buy a house. If you really want to keep your monthly payment to an absolute minimum, do whatever is necessary to get the highest credit score you can.

If you’re a first-time homebuyer, you’re probably going to buy a house with a minimum down payment. And if you do, you’ll need to pay PMI. That being the case, a low credit score will result in a higher mortgage payment itself, as well as on the PMI premium.

Spending some time and effort to improve your credit score is one of the best long-term investments you can make. And if you’re already in your home and looking to refinance, you can use the same strategies spelled out in this article to improve your credit score for a new loan. The same rules applied – the higher your credit score is, the lower your interest rate, PMI, and monthly payment will be.

You owe it to yourself to make the extra effort.

Refinancing an Auto Loan: How to Know If It’s a Good Idea

Reverse Mortgages Pros and Cons: Ripoff or a Good Idea?

8 Ways it Just Got Easier to Achieve Student Loan Forgiveness

15 Smart Strategies for Planning a Move During COVID-19

Term vs. Whole Life Insurance: Why Term is Almost Always Better

PrivacyGuard Review

Orchard Bank Credit Cards | NOT a Scam!

What is CitiCards CBNA On My Credit Report

What is BRCLYSBANKDE on My Credit Report?