Credit

5 Amazingly Simple Techniques to Optimize Your Credit Score

Forget maxing out your credit cards, here are some easy techniques anyone can use to max out your credit score.

Most of these techniques can be used by those who have both good and bad credit.

I recommend that you try to do as many as possible on an ongoing basis.

5 Amazingly Simple Credit Optimization Techniques

Here are 5 simple techniques that you can use to optimize your credit score:

- Limit Hard Inquiries

- Keep a Mixture of Credit Accounts

- Optimize Your Credit Utilization Ratio

- Open a Major Credit Card

- Build Your Credit History

1. Limit Hard Inquires to No More Than 2 During a 2 Year Period

There are two types of credit inquiries that might show up on your credit report. One can negatively affect your credit score, and one doesn’t.

- Soft Inquiry: This type of inquiry will not negatively affect your credit score so you shouldn’t worry about these. Examples of soft inquiries are when you check your credit report, an employer pulls your credit report, or when you use a credit monitoring service.

- Hard Inquiry: This type of inquiry can impact your credit score (but not always). Examples of hard inquiries are when you apply for a credit card, a car loan, etc.

The main thing to keep in mind when it comes to credit inquiries is that a hard inquiry means you are applying for credit, while a soft inquiry is simply you (or someone else) looking at your credit report for reasons other than loaning you money.

So, how many inquiries is too many? As a general rule, you should keep hard inquiries under 2 during any given two year period. Hard inquiries fall off your credit report after two years.

This basically tells lenders that you aren’t actively looking for a bunch of credit. You may start to see your credit score negatively affected once you hit three or more hard inquiries.

Having more than two hard inquiries won’t kill your credit score, but it will likely take a few points off.

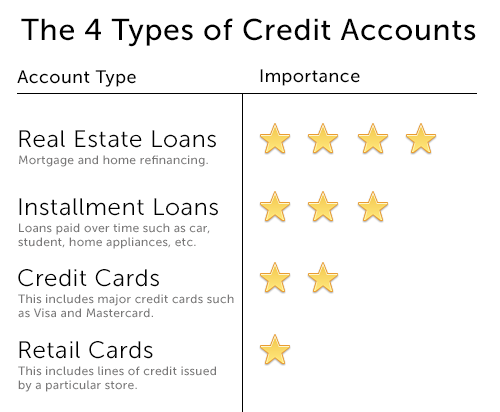

2. Keep a Mixture of Credit Account Types

There are 4 types of credit accounts on your credit report and the type of account determines how much of an impact it has on your credit score.

I put together the graphic below to show you which types matter the most:

It’s best to keep a mixture of all these account types. It doesn’t mean that you should close your retail cards, it simply means that a real estate loan will more than likely have a bigger impact on your credit score than a retail card or credit card.

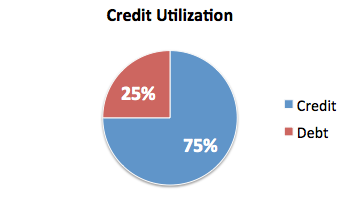

3. Use Credit Utilization Ratios to Your Advantage

Maxing out your credit cards will kill your credit score really fast. Credit vs. Debt ratios are something people often overlook.

Most people think that their credit score isn’t impacted unless they are late on a payment.

This isn’t true! In fact, I would suggest keeping each credit card under 25% utilization. In other words, don’t charge up more than 25% of your available credit on any particular card.

If you have already charged more than 25%, paying it down to under 25% can significantly increase your score. I have written an entire article about credit utilization that you should check out if you want to understand it more in depth.

4. Open at Least One Major Credit Card

This one can sometimes be difficult for people who have bad credit, but it should be something you work towards in the long run.

Since major credit card companies usually require decent credit to approve you for one of their credit cards, having one (or a few) shows that they trust you.

This will positively affect your credit score. Again, if you have bad credit, simply keep this in mind and work towards getting to the point where you can get approved for a Visa or Mastercard.

I should also mention that if you don’t have any credit, sometimes major credit card companies will approve you. Consider this your trial period and don’t screw it up

5. Grow Your Credit History by Keeping Old Accounts Open

A mistake that I see people do again and again (and one I did myself, actually) is close old accounts thinking that it will improve their credit score.

A person usually does this because the old account has a late payment or something. The truth is, this isn’t going to make the late payment “go away” –it will still be there.

What you will do by closing an old account is to stop building history for that account.

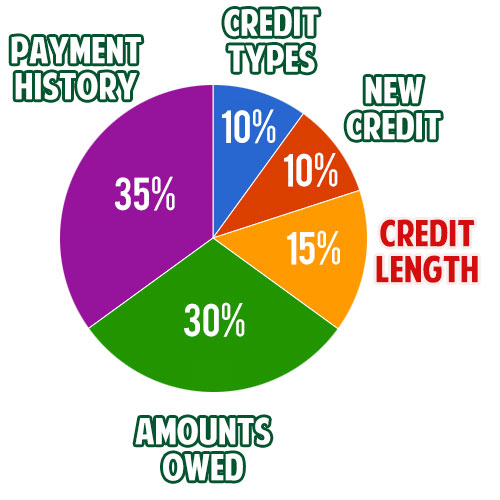

There are several factors used to calculate your credit score (see chart below), and your credit length makes up a significant portion: 15%.

By keeping old accounts open, the account continues to build credit history and this is a good thing! In the long run, your credit score will usually benefit.

Optimize Your Credit Report

Lastly, you should also always spend some time cleaning up your credit report by removing any collections or late payments. I recommend getting negative entries removed rather than wait 7 years for them to automatically fall off.

This way you don’t have to worry about them affecting your ability to get a loan.

I suggest you check out Lexington Law Credit Repair. They’ll remove the negative items. Give them a call at 1-844-764-9809 or Check out their website.

Refinancing an Auto Loan: How to Know If It’s a Good Idea

Reverse Mortgages Pros and Cons: Ripoff or a Good Idea?

8 Ways it Just Got Easier to Achieve Student Loan Forgiveness

15 Smart Strategies for Planning a Move During COVID-19

Term vs. Whole Life Insurance: Why Term is Almost Always Better

PrivacyGuard Review

Orchard Bank Credit Cards | NOT a Scam!

What is CitiCards CBNA On My Credit Report

What is BRCLYSBANKDE on My Credit Report?